How to Verify Insurance Psychiatric Care Coverage

- joeudesign

- May 20

- 8 min read

Getting psychiatric care should not start with a guessing game about what your insurance will actually pay. Yet for millions of Americans, that is exactly what happens. To verify insurance psychiatric care coverage before your first appointment is one of the most financially protective steps you can take, and most people skip it entirely. With about 22.8% of U.S. adults experiencing mental illness in 2021, the demand for clear, accessible psychiatric coverage has never been higher. This guide walks you through every step.

Table of Contents

Key takeaways

Point | Details |

Verify before your first visit | Confirming coverage before treatment begins prevents surprise bills and claim denials. |

Know your specific cost details | Ask about deductibles, copays, session limits, and prior authorization requirements. |

Telehealth coverage is active | Medicare telehealth flexibilities for mental health are extended through December 31, 2027. |

You can fight denials | A letter of medical necessity from your clinician is a powerful tool to challenge coverage refusals. |

Document everything | Keep written records of every call, portal search, and confirmation you receive from your insurer. |

What you need before verifying psychiatric care coverage

Before you pick up the phone or log into your insurer’s portal, gather a few things. Walking into this process unprepared wastes time and can lead to incomplete answers that cost you later.

Start with these materials:

Your insurance card, which has your member ID, group number, and the member services phone number

Your Summary of Benefits and Coverage (SBC), usually available through your insurer’s online portal or your employer’s HR department

The name, NPI number, and practice address of any psychiatric provider you are considering

A notepad or open document to record names, dates, and reference numbers from every conversation

Beyond the paperwork, you need to understand a few basic insurance terms before you call. A deductible is the amount you pay out of pocket before your insurance starts covering costs. A copay is a fixed fee per visit. Coinsurance is the percentage you pay after meeting your deductible. And in-network means the provider has a contract with your insurer, which almost always means lower costs for you.

You also need to know which types of psychiatric services you want to ask about. These include outpatient therapy, psychiatric medication management, telehealth visits, intensive outpatient programs (IOP), and inpatient psychiatric care. Each may have different coverage rules, so being specific when you call gets you more accurate answers.

Pro Tip: Before calling, write down at least five questions you want answered. Insurance representatives move fast, and having your questions written out prevents you from forgetting something that matters.

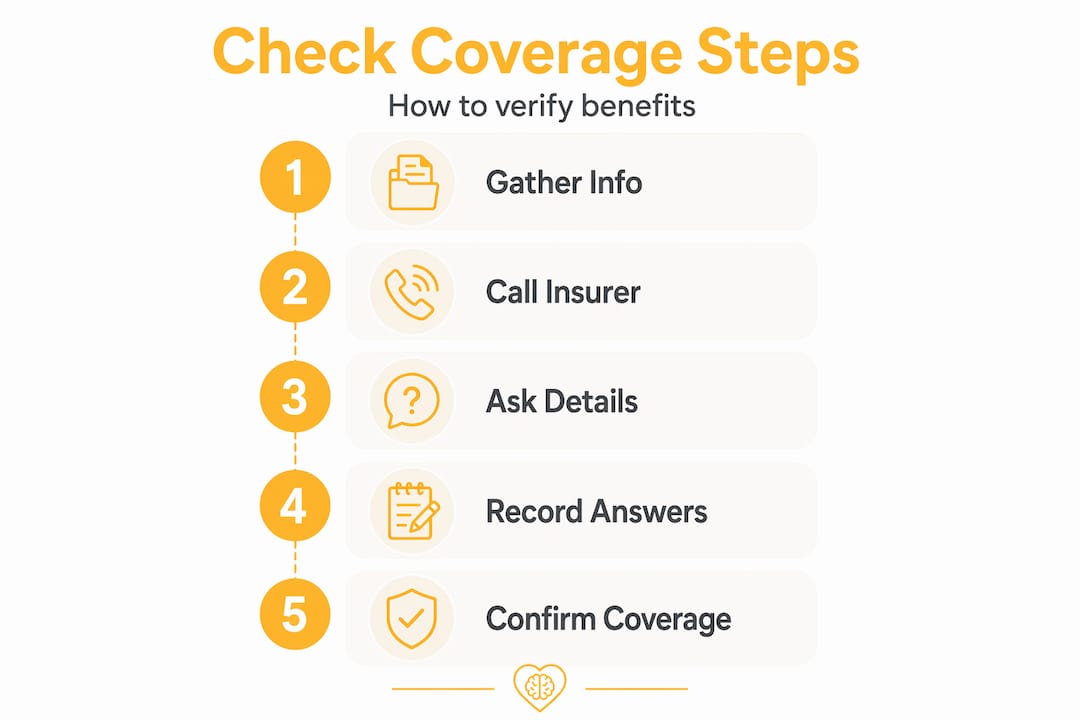

Step-by-step: how to verify insurance psychiatric care coverage

Patient eligibility verification should happen before you receive any psychiatric care. Here is exactly how to do it.

Call member services. Use the phone number on the back of your insurance card. Tell the representative you want to verify your mental health and psychiatric benefits. Ask for a reference number at the start of the call and write it down.

Ask about in-network status. If you already have a provider in mind, give them the provider’s name and NPI number. Ask directly: “Is this provider in-network under my current plan?” If you do not have a provider yet, ask how to search for in-network psychiatrists in your area.

Ask your core coverage questions. Specifically, you want to know: What is my deductible for mental health services? What is my copay or coinsurance per visit? Is there an annual session limit? Does my plan require prior authorization for psychiatric care or medication management?

Confirm telehealth coverage. Ask whether telehealth psychiatric visits are covered and at what rate. Medicare telehealth flexibilities for mental health services are extended through December 31, 2027, but private plan rules vary.

Use the online portal as a second check. Log into your insurer’s member portal and search for mental health benefits under your plan documents. Cross-reference what the representative told you with what the portal shows. Discrepancies happen, and catching them early protects you.

Get written confirmation. Ask the representative to send a summary of what was discussed, or take a screenshot of the portal information. If a dispute arises later, written records are your best defense.

Contact the provider’s billing office. After verifying with your insurer, call the psychiatric practice directly and ask them to run a benefits check on your behalf. Providers do this regularly and can catch details you may have missed.

Pro Tip: Always ask the insurance representative for their employee ID or name, the date and time of the call, and a reference number. If your claim is ever denied, this information becomes critical evidence.

Common obstacles when verifying psychiatric insurance coverage

Even when you follow every step correctly, you will sometimes run into walls. Here is how to handle the most common ones.

No in-network providers available. This is more common than most people realize. Despite parity laws, many patients face limited in-network mental health access and end up paying high out-of-pocket costs because of network gaps. If your insurer’s network does not include an available psychiatrist, you can request out-of-network coverage at in-network rates by documenting your failed attempts to find an in-network provider. Some states legally require insurers to grant this when network adequacy standards are not met.

Denials citing “medical necessity.” Insurers sometimes deny claims by arguing the treatment is not medically necessary. Your most effective response is a letter of medical necessity from your clinician. Letters of medical necessity can be submitted before treatment begins or after an initial denial, and they carry significant weight in the appeals process.

Coverage disputes that do not resolve. When direct conversations with your insurer go nowhere, escalate. State insurance regulators and employers can step in to assist with complaints or negotiate access issues. Filing a formal complaint with your state’s insurance department creates a paper trail and often prompts faster responses from insurers.

Keep a dedicated log of every interaction with your insurer. Include the date, time, representative’s name, reference number, and a summary of what was said. This log is your most valuable asset if a dispute escalates.

Track your communications the same way you would track a legal case, because sometimes that is exactly what it becomes.

Verifying costs, session limits, and telehealth options

Once you confirm that psychiatric care is covered, you need to understand the financial specifics. The difference between a $30 copay and a 30% coinsurance after a $2,000 deductible is enormous, and both technically count as “covered.”

Coverage detail | What to ask your insurer |

Deductible | Has my deductible been met? Does it apply to mental health visits separately? |

Copay vs. coinsurance | Do I pay a flat copay per visit or a percentage after the deductible? |

Out-of-pocket maximum | What is my annual cap on mental health spending? |

Session limits | Does my plan cap the number of outpatient psychiatric visits per year? |

Inpatient coverage | What does my plan cover for inpatient psychiatric stays, and for how long? |

Telehealth parity | Are telehealth psychiatric visits covered at the same rate as in-person visits? |

Individual therapy sessions can cost between $100 and $250 without insurance, which makes understanding your exact cost-sharing structure critical for budgeting. A plan with a high deductible and coinsurance could leave you paying close to full price for months.

The Affordable Care Act requires most small group and individual health plans to cover mental health services as essential benefits with parity to medical coverage. But parity in law does not always mean parity in practice. Session limits, prior authorization requirements, and narrow networks can all reduce your effective access even when coverage technically exists.

Pro Tip: Ask specifically whether your plan covers intensive outpatient programs (IOP) and partial hospitalization programs (PHP). These levels of care sit between standard outpatient therapy and inpatient hospitalization, and coverage for them varies widely.

What to do after verifying your coverage

Verification is not a one-time event. It is the start of an ongoing process. Here is what to do once you have confirmed your benefits.

Confirm details with your provider before the first appointment. Share what your insurer told you and ask the provider’s billing team to verify it independently. Billing errors and outdated information are common.

Keep all verification records. Save screenshots, emails, and your call log in a dedicated folder. You may need them months later if a claim is denied.

Prepare for prior authorization if required. Some plans require pre-approval before psychiatric care begins. Ask your provider to initiate this process early, as it can take days or weeks.

Re-verify at plan renewal. Your benefits can change every year. If your plan renews in January, re-check your mental health benefits in December.

Re-verify when your provider changes. If your psychiatrist leaves a practice or your insurer updates its network, your in-network status can change without notice.

Know your appeals rights. If a claim is denied after treatment, you have the right to appeal. Your insurer must provide written explanation of any denial, and you have a defined window to respond.

My honest take on navigating psychiatric insurance

I have seen people delay psychiatric care for months because they were afraid of what it would cost. Then they finally verify their insurance and discover their copay is $30 a visit. The fear was worse than the reality, and the delay caused real harm.

But I have also seen the opposite. Someone assumes their plan covers everything, starts treatment, and receives a $1,800 bill three months later because they never confirmed prior authorization. Both situations are preventable.

What I have learned is that insurance verification is not a bureaucratic formality. It is an act of self-advocacy. The system is genuinely confusing, and insurers do not always make it easy to get clear answers. But the people who push through that confusion, ask specific questions, and document their calls are the ones who get the care they need without financial catastrophe.

My approach: treat every insurance call like a job interview. Prepare your questions, take notes, and follow up in writing. The extra 20 minutes you spend on verification can save you thousands of dollars and weeks of unnecessary stress.

— Martin

Start your care with confidence at 2ndarc

If you have done the work to verify your benefits and you are ready to move forward, 2ndarc is built to make the next step straightforward. 2nd Arc Psychiatric Associates accepts most major insurance plans and offers both in-person and telehealth psychiatric services across New York, with appointments often available within 24 hours. The team handles personalized care for anxiety, depression, ADHD, and more, and they can help clarify your insurance benefits before your first visit. Whether you are seeking psychiatric care in New York or want to understand your coverage options before committing, 2ndarc is ready to help you get started without the guesswork.

FAQ

What does it mean to verify insurance psychiatric care coverage?

Verifying insurance psychiatric care coverage means confirming with your insurer that psychiatric services are covered under your plan, including specific details like copays, deductibles, session limits, and prior authorization requirements before you begin treatment.

How do I check my mental health insurance benefits?

Call the member services number on the back of your insurance card and ask specifically about mental health and psychiatric benefits. You can also log into your insurer’s online portal to review your Summary of Benefits.

Does insurance cover telehealth psychiatric visits?

Many plans cover telehealth psychiatric visits, and Medicare telehealth coverage for mental health services is extended through December 31, 2027. Private plan rules vary, so confirm telehealth parity directly with your insurer.

What should I do if my insurance denies psychiatric care?

Request a letter of medical necessity from your clinician and submit a formal appeal. If the denial is not resolved, you can file a complaint with your state’s insurance regulator for additional support.

How often should I re-verify my psychiatric coverage?

Re-verify your mental health insurance benefits at every plan renewal, typically once a year, and any time your provider changes or you switch insurance plans.

Recommended

Comments